- Mobile:+8801787433263, +8801819295664

- Email : info@mohabbatgarments.com

-

Sat-Thu : 9AM-6PM

As the global fashion industry navigates trade tensions and rising protectionism, particularly under the Trump administration’s “reciprocal” tariffs, countries like Australia are being forced to re-evaluate their dependency on offshore manufacturing, while nations like Bangladesh may stand to gain amid the shifting landscape.

Dale McCarthy, founder of luxury swimwear brand Bondi Born, is one of many Australian entrepreneurs caught in the crosshairs of geopolitical trade policies.Her brand, which previously relied on manufacturers in China and Vietnam, is now pivoting to Portugal and exploring limited local production in Australia.

Escalating U.S. tariffs on Chinese-made goods have rendered her international supply chain increasingly risky and volatile.

“The quality is just as good, and the cost of making swimwear in Vietnam was a third of what it would be in Australia,” said McCarthy. But the uncertainty caused by fluctuating tariffs has forced her to reconsider the model.

While Australia’s domestic manufacturing capability has eroded over the past three decades — with just 3% of local brands' clothing made in Australia — Bangladesh has steadily built itself into a global garment powerhouse, with exports exceeding $45 billion annually and contributing over 11% to the country’s GDP.

Opportunity for Bangladesh amid global realignment

As fashion brands in Western countries, including Australia, seek alternatives to China amid rising costs and political uncertainties, Bangladesh's value proposition becomes stronger. The country’s competitive labor market, growing sustainable manufacturing ecosystem, and government-backed special economic zones make it a favorable destination for relocation or expansion.

Already, major global brands have begun diversifying sourcing, with Bangladesh topping their list for categories like knitwear, lingerie, sportswear, and outerwear — segments where skilled craftsmanship and vertical integration matter.

Bangladesh's skilled workforce vs. Australia’s manufacturing gap

One of the main hurdles Australian brands face in reshoring production is a shrinking pool of skilled garment workers, with the average age of those in the trade sitting at 57, according to Dr. Harriette Richards of RMIT University. In contrast, Bangladesh boasts a youthful, predominantly female workforce, supported by vocational training initiatives and factory-based skill-building programs.

Moreover, Bangladesh’s rise as a hub for sustainable and circular fashion further enhances its appeal to international buyers concerned about ESG standards. Initiatives like green factories, solar-powered industrial parks, and compliance with global labor standards have helped transform its global image.

Australia eyes strategic revival — But not for fast fashion

Recognizing the long-term decline of domestic manufacturing, the Australian Fashion Council (AFC), in collaboration with brands like RM Williams, has launched a national strategy to revive garment production, focusing on high-end, sustainable, “investment” pieces rather than low-cost fast fashion.

“We shouldn’t compete on $2 products,” said AFC CEO Jaana Quaintance-James. “This is about quality pieces made in Australia, with transparency and skill.”

But for most Australian fashion businesses, especially SMEs, local production is economically unsustainable. As tariffs squeeze China and neighboring suppliers, Bangladesh stands out as a bridge between quality, scale, and cost-efficiency.

Global fashion at a crossroads

Dr. Richards warns that the fashion industry's global system — built on fast fashion and low consumer prices — has created a distorted perception of value.

“We’ve moved far away from understanding how clothes are made, how skilled the work is, and why quality comes at a price.”

Bangladesh’s positioning now gives it a rare opportunity — not just to capture business from China but also to lead a new chapter in ethical and resilient fashion manufacturing.

As Australia grapples with rebuilding its local capabilities, Bangladesh is ready to absorb shifting demand. The question is no longer whether global production will move — but where to, and how fast.

Tariff tensions reshape global fashion supply chains

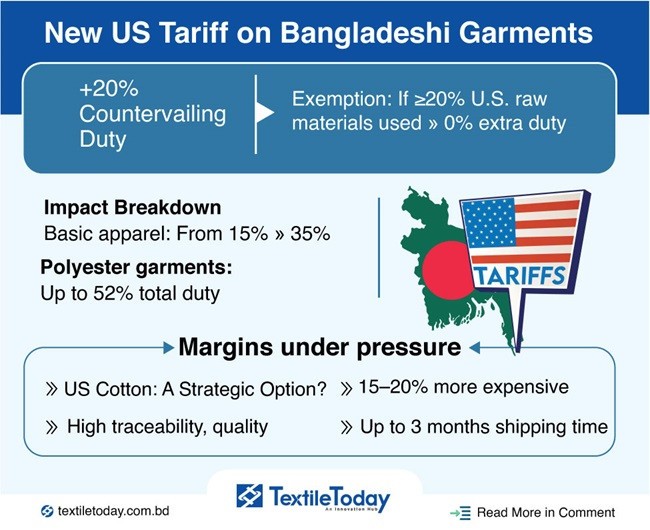

Bangladesh apparel eyes U.S. market despite costly cotton route